e-Invoicing FAQs

1. Is e-Invoicing mandatory for all businesses in Malaysia?

Yes, e-Invoicing will become mandatory for all businesses, with the implementation dates varying based on the company's annual turnover thresholds as outlined above.

2. How can businesses prepare for e-Invoicing implementation?

Businesses should:

- Assess and upgrade their accounting and invoicing systems to ensure compatibility with e-Invoicing requirements.

- Train staff on new processes and compliance obligations.

- Consult with tax professionals or service providers specialising in e-Invoicing solutions.

3. Are there any exemptions to e-Invoicing requirements?

Certain entities, such as individuals not conducting business and taxpayers with annual turnover below RM1 million, may be exempt. However, note that the exemption does not apply if your business has a non-individual shareholder, is a subsidiary, or has a related company/JV partner with annual turnover of RM1 million or more. It's essential to consult the latest guidelines from IRBM for specific exemption conditions. Check out our comprehensive article for e-Invoicing exemptions in Malaysia.

4. What is the e-Invoicing treatment during the interim relaxation period?

Taxpayers are generally given a six (6) month interim relaxation period from their mandatory implementation date. However, Phase 4 taxpayers (annual turnover RM1 million to RM5 million) have been granted an extended relaxation period until 31 December 2027, following the government's April 2026 announcement. Full penalty enforcement for Phase 4 will begin on 1 January 2028.

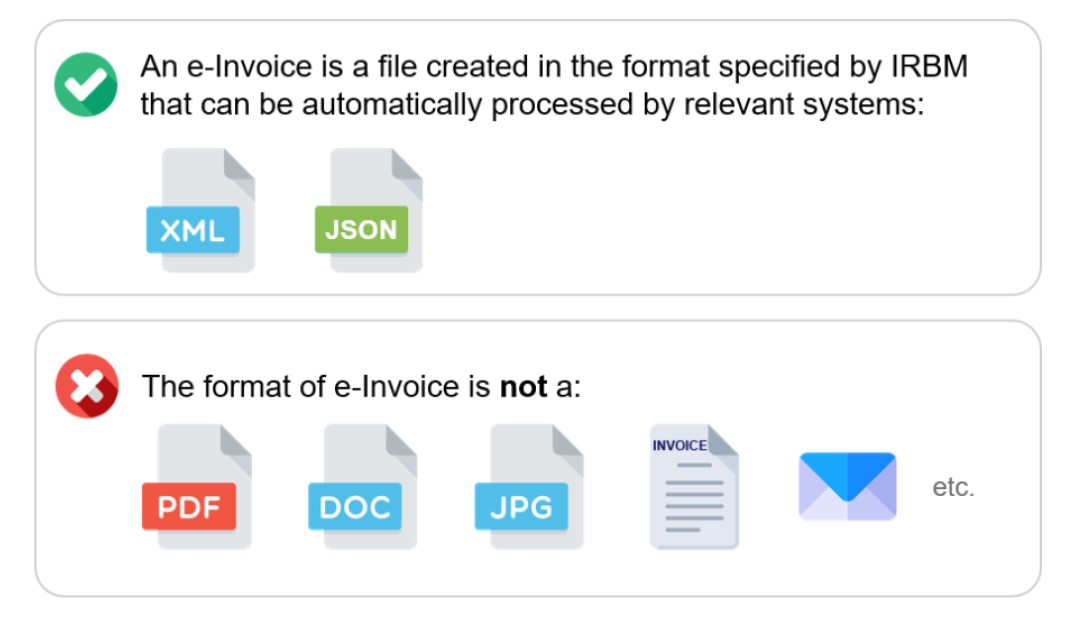

5. What formats are accepted for e-Invoices in Malaysia?

The IRBM accepts e-Invoices in XML or JSON formats, adhering to the Universal Business Language (UBL) 2.1 standard.

6. How will e-Invoicing affect cross-border transactions?

While e-Invoicing primarily targets domestic transactions, businesses engaged in international trade should stay informed about any additional requirements or guidelines issued by the IRBM.

7. What support is available for businesses transitioning to e-Invoicing?

The IRBM provides guidelines, FAQs, and a Software Development Kit (SDK) to assist businesses. Additionally, consulting with tax professionals or e-Invoicing solution providers like BDO can facilitate a smoother transition for your business.

8. What are the consequences of non-compliance with e-Invoicing regulations?

Non-compliance may result in penalties, fines, or other enforcement actions by the IRBM. It's crucial for businesses to adhere to the implementation timelines and requirements to avoid such consequences.

9. How long should I keep e-Invoices for tax purposes?

The IRBM typically requires businesses to retain financial records, including invoices, for a specified period (usually 7 years) for tax audits and compliance purposes.

10. Can I submit e-Invoices in bulk, or do I need to upload each invoice individually?

The MyInvois system and most e-Invoicing platforms allow for bulk submissions, which can save time for businesses handling high volumes of transactions. See how our e-Invoice Middleware can help.

11. How does e-Invoicing benefit SMEs specifically?

For SMEs, e-Invoicing can streamline invoicing processes, reduce administrative costs, and ensure compliance with tax regulations. It also levels the playing field by allowing smaller businesses to operate with the same efficiency as larger companies.

12. How does e-Invoicing align with environmental sustainability goals?

e-Invoicing reduces the need for paper invoices, lowering your business's paper consumption and contributing to environmental sustainability. It also cuts down on storage requirements, reducing physical waste and promoting a greener business operation.

13. What are the rules for e-Invoices issued in foreign currency?

Effective 31 March 2026, under Public Ruling No. 01/2026 issued by the Royal Malaysian Customs Department (RMCD), businesses that issue service tax or sales tax invoices in a foreign currency must also state the equivalent amount in Malaysian Ringgit (MYR). The exchange rate used must be sourced from an approved reference, such as Bank Negara Malaysia, any BNM-registered commercial bank, or international agencies like Bloomberg, Reuters, or Oanda, and must be applied consistently for at least one year. For the MyInvois system specifically, the "Currency Exchange Rate" field is mandatory on all foreign-currency e-Invoices; invoices with missing or incorrect exchange rate data will be rejected by IRBM.

.jpg)

.jpg)

-(2).png)

-(4).png)